Ask any experienced investor what the hardest part of investing is, and most will give you the same answer: timing.

Buying at the bottom and selling at the top sounds simple in theory. In practice, it's nearly impossible — even for professionals with decades of experience and access to the best tools in the world. The data backs this up: the vast majority of actively managed funds underperform simple index strategies over the long run, largely because of failed attempts to time the market.

Dollar-cost averaging (DCA) is the antidote to that problem. It doesn't try to outsmart the market. It removes the timing decision entirely — and in doing so, it removes most of the emotion from investing too.

This article is for educational purposes only and does not constitute financial advice. All investments carry risk. Always conduct your own research before making any financial decisions.

Jump To:

- Terms To Know

- What Is Dollar-Cost Averaging?

- A Concrete Example of DCA Investing

- Why DCA Makes Sense

- Who Uses DCA and Why

- DCA Across a Mixed Portfolio — Crypto and Stocks

- Interactive DCA Allocator

- How to DCA in a Self-Custodial Wallet

- Interactive DCA Calculator

- Common DCA Mistakes

Terms To Know

What Is Dollar-Cost Averaging?

Dollar-cost averaging is the practice of investing a fixed amount of money into an asset at regular intervals, regardless of what the price is doing at the time.

That's it. Every week, every two weeks, every month — you invest the same amount. When the price is high, your fixed amount buys fewer units. When the price is low, it buys more. Over time, your average cost per unit smooths out across the highs and lows of the market, rather than being locked in at whatever the price happened to be on the one day you decided to invest.

The key concept here is average cost basis — the average price you've paid per unit across all your purchases. DCA is designed to keep your cost basis reasonable over time, without requiring you to predict where the market is going.

A Concrete Example of DCA Investing

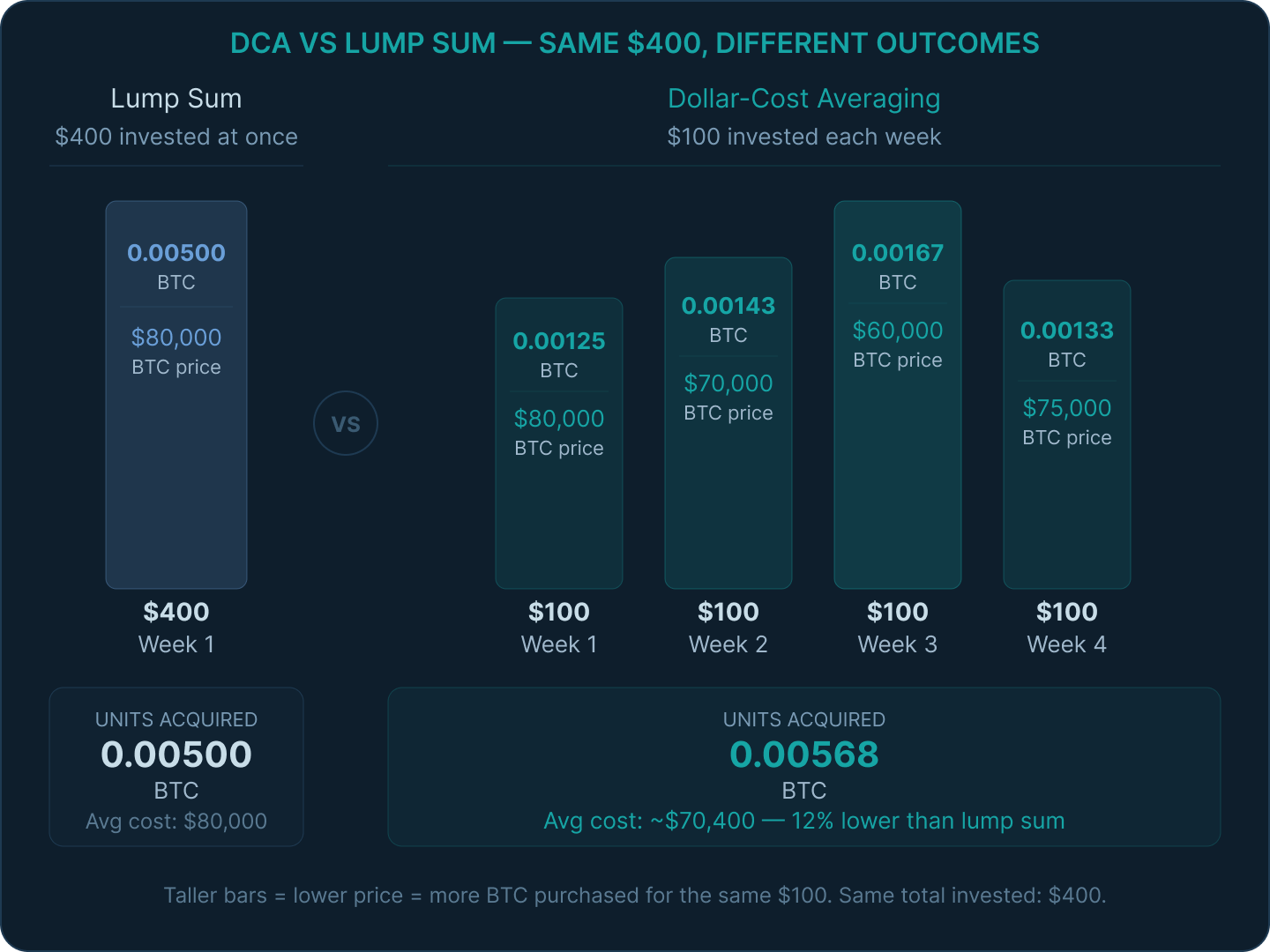

Let's say you invest $100 in Bitcoin every week for four weeks. Here's what that might look like:

Total invested: $400. Total BTC purchased: 0.00568 BTC. Average cost per BTC: approximately $70,400.

Now compare that to someone who invested all $400 in week one at $80,000. They'd have 0.005 BTC at an average cost of $80,000 per coin.

The DCA investor bought more during weeks two and three when prices were lower, bringing their average cost down significantly — without needing to predict that prices would fall. The discipline of investing consistently did that automatically.

Why DCA Makes Sense

It removes emotion from the equation. The biggest enemy of good investing isn't the market — it's the investor's own psychology. Fear causes people to sell at the bottom. Greed causes them to buy at the top. FOMO drives impulsive decisions. DCA sidesteps all of that by replacing decision-making with a schedule. You don't ask "should I buy now?" — you just buy, because it's Tuesday and that's what you do on Tuesdays. It also reduces the urge to panic sell — when your cost basis is spread across many purchases at different prices, there's no single entry point to fixate on and compare against the current price.

Nobody consistently times the market. There's a reason the phrase "time in the market beats timing the market" has become a cliché — it's because the evidence is overwhelming. Missing just a handful of the best trading days in any given year can devastate your returns. DCA keeps you invested consistently, which means you're always there for the good days, not just the bad ones.

Volatility works in your favor. This is the counterintuitive part of DCA that most people miss. In highly volatile markets — like crypto — price swings actually help the DCA investor. When prices drop sharply, your fixed investment amount buys significantly more units. When prices recover, those extra units gained during the dip amplify your returns. Volatility stops being something to fear and starts being something that works for you.

It builds a habit. Consistently setting aside money to invest, on a schedule, trains a financial discipline that compounds over time. The investor who puts in $200 a month for five years will almost certainly outperform the one who waits for the "right moment" and never pulls the trigger.

Who Uses DCA and Why

DCA isn't a strategy for any one type of investor — it's used across the full spectrum.

Long-term holders use it to build positions in assets they believe in without trying to pick entry points. Whether they're accumulating Bitcoin, Ethereum, or a basket of tokenized stocks, the goal is the same: build exposure over time at a reasonable average cost.

Regular income earners often find DCA the most natural fit. Investing a percentage of each paycheck — automatically, on payday — turns savings into investment without requiring active thought or discipline each time.

New investors entering volatile markets use DCA to manage their anxiety about getting the timing wrong. If you're allocating a significant sum to crypto for the first time, spreading it across several months of purchases is far less psychologically stressful than deploying it all at once — and historically, it often produces better outcomes too.

Investors rebalancing or building across multiple asset classes use DCA to grow different parts of their portfolio at different rates, depending on their target allocation and current market conditions.

DCA Across a Mixed Portfolio — Crypto and Stocks

Most DCA content focuses on a single asset or a single asset class. But for investors managing a portfolio that includes both crypto and tokenized stocks — increasingly common for self-custodial wallet users — the strategy becomes more nuanced and more powerful.

Different assets, different volatility profiles. Bitcoin and Ethereum are significantly more volatile than tokenized US equities. That volatility makes DCA more impactful for crypto — the price swings are larger, so the averaging effect is more pronounced. For tokenized stocks, the volatility is lower but the long-term compounding of reinvested dividends and steady growth makes consistent accumulation just as valuable.

You can DCA across all of them simultaneously. A self-custodial wallet that holds both crypto and tokenized stocks lets you apply the same consistent investment discipline across every asset class you care about — without needing separate brokerage accounts, separate platforms, or separate schedules. One wallet, one strategy, multiple assets.

Stablecoins as the starting point. In a self-custodial wallet, DCA typically works by holding a reserve of stablecoins — USDC, for example — and swapping a fixed amount into your target assets on your chosen schedule. The stablecoin acts as your "dry powder," ready to be deployed into BTC, ETH, tokenized Apple, or whatever else is on your list at your predetermined intervals.

Consider your allocation targets. DCA doesn't mean buying the same assets in the same proportions forever. If your target allocation is 40% blue chips, 20% altcoins, 25% stables, and 15% tokenized RWAs, your regular DCA purchases should reflect those targets — or be adjusted to bring your actual allocation back in line with them. This is where DCA and portfolio rebalancing work together. For more on how to think about allocation targets, see our article on Asset Allocation & Portfolio Rebalancing.

Interactive DCA Allocator

Try our Interactive DCA Allocator for yourself:

How to DCA in a Self-Custodial Wallet

DCA in a self-custodial wallet is more manual than setting up an automatic investment plan with a traditional broker — but it gives you full control over your assets at every step.

Step 1 — Set your budget and interval Decide how much you'll invest per period and how often. Weekly, biweekly, and monthly are the most common. Be realistic — the amount should be one you can commit to consistently without straining your finances, including during downturns.

Step 2 — Define your target assets Which assets are you DCAing into? Be specific. "Crypto" is not a DCA plan. "50% BTC, 30% ETH, 20% tokenized S&P 500 exposure" is a DCA plan. Have a thesis for each asset — you should be buying it because you believe in it long term, not because it's popular this week.

Step 3 — Keep a stablecoin reserve In a self-custodial wallet, your DCA capital typically sits in stablecoins between purchases. Maintain a balance of USDC or a similar asset ready to deploy on your schedule.

Step 4 — Execute your swaps on schedule On your chosen day, swap the predetermined stablecoin amount into your target assets using the swap function in your wallet. Keep the intervals consistent — the discipline of the schedule is what makes DCA work.

Step 5 — Keep records Every swap is a taxable event in most jurisdictions. Keep a log of each purchase: date, amount in stablecoins, asset purchased, units received, and the price at the time. This makes tax reporting significantly easier and gives you a clear picture of your average cost basis over time.

Step 6 — Review periodically, but don't tinker constantly DCA is a long-term strategy. Check in quarterly to make sure your allocation still matches your targets and adjust if necessary — but resist the urge to change your strategy every time the market moves. The whole point is consistency.

Interactive DCA Calculator

Try our Interactive DCA Calculator yourself:

Historical price data sourced from Yahoo Finance. Calculations use approximate monthly close prices. Current prices as of June 17, 2026. Past performance is not indicative of future results.

Common DCA Mistakes

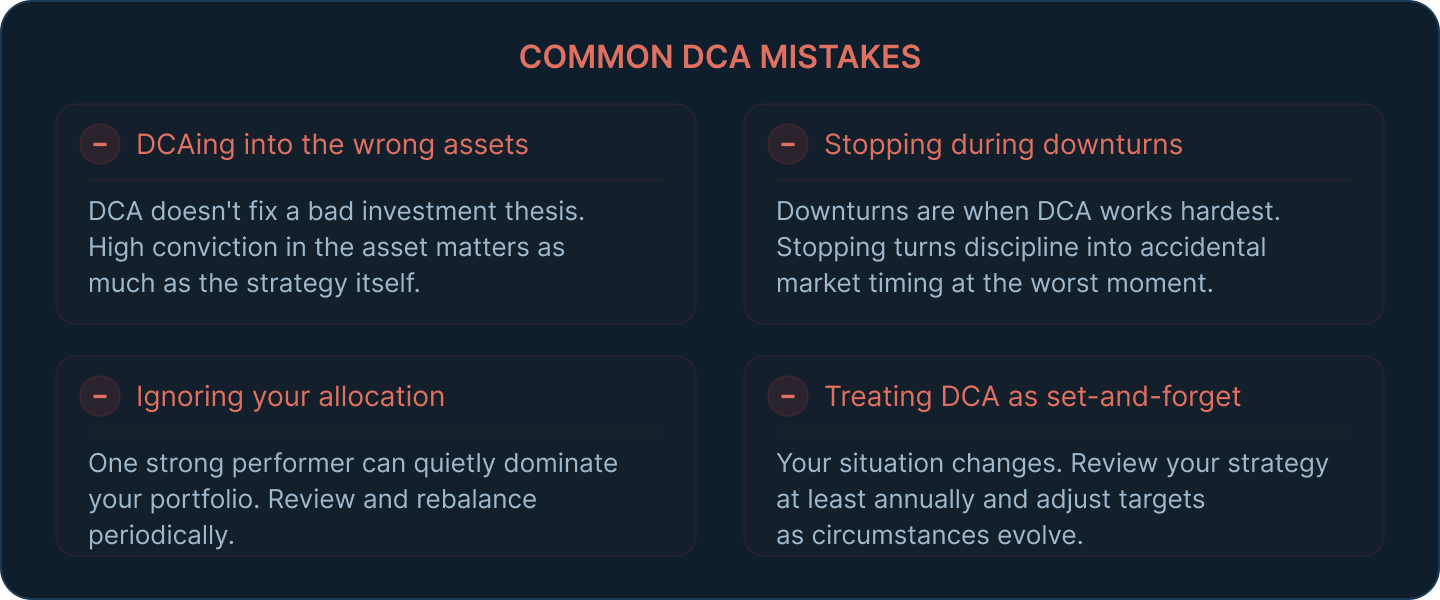

DCAing into the wrong assets. DCA is a strategy for building a position over time — it doesn't fix a bad investment thesis. Consistently buying an asset you don't understand, or one with weak fundamentals, just means you accumulate more of a bad investment at a lower average cost. High conviction in the asset matters as much as the strategy itself.

Stopping during downturns. This is the most common and most costly mistake. When prices fall sharply, the natural human instinct is to stop investing — or worse, to sell. But downturns are exactly when DCA is doing its most valuable work, buying more units for the same amount of money. Stopping during a bear market turns a disciplined strategy into an accidental market-timing attempt.

Ignoring your overall allocation. DCA without attention to allocation can gradually create an imbalanced portfolio. If one asset outperforms significantly, it will grow to dominate your holdings even if you're buying everything equally. Review your allocation periodically and adjust your DCA purchases to keep your portfolio in line with your targets.

Treating DCA as set-and-forget forever. DCA is a long-term strategy, not a permanent autopilot. Your financial situation, risk tolerance, and investment thesis can change. Review your strategy at least annually and be willing to adjust your targets, amounts, or asset selection as your circumstances evolve.

Thank you for checking out our What is Dollar-Cost Averaging article! Make sure to follow us on X(Twitter) and let us know your thoughts. Subscribe to our newsletter to stay up to date with MEW releases, and check out our weekly podcast Crypto Currents for the latest news in crypto. For more on building and managing a portfolio, check out our articles on Asset Allocation & Portfolio Rebalancing and Tokenized Stocks.